¡Tu solución está lista!

Nuestra ayuda de expertos desglosó tu problema en una solución confiable y fácil de entender.

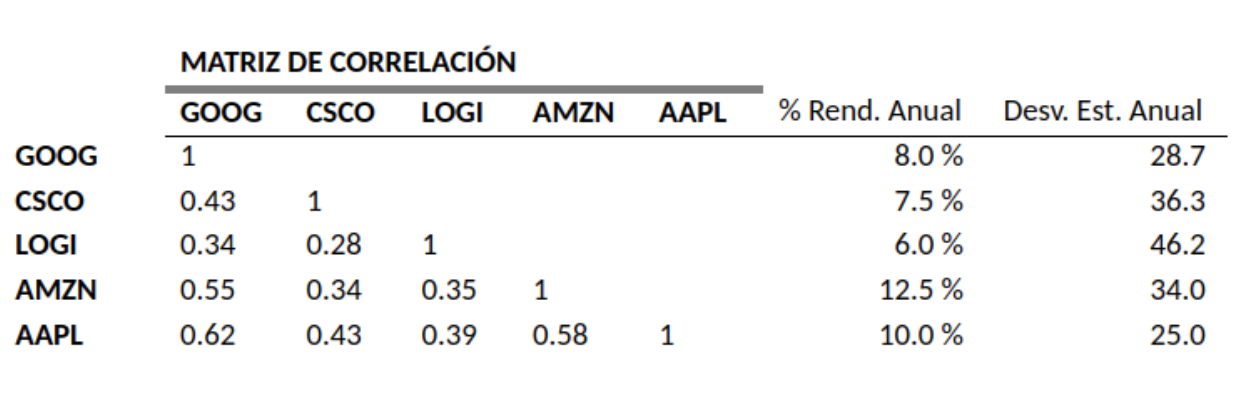

Mira la respuestaMira la respuesta done loadingPregunta: You decide to invest your money in a stock portfolio that is 60% Cisco Systems and 40% Amazon.com. USING THE FOLLOWING PROPERTIES:

You decide to invest your money in a stock portfolio that is 60% Cisco Systems and 40% Amazon.com.

USING THE FOLLOWING PROPERTIES:

FIND THE STANDARD DEVIATION OF THE PORTAFOLIO

Queda solo un paso para resolver este problema.SoluciónPaso 1Mira la respuesta completa

Queda solo un paso para resolver este problema.SoluciónPaso 1Mira la respuesta completaWe have been given that we invest 60% in Cisco and 40% in Amazon.

We have to calculate standard devia...

Respuesta Desbloquea

Desbloquea

Texto de la transcripción de la imagen:

MATRIZ DE CORRELACIÓN \begin{tabular}{llllrrrrr} & GOOG & CSCO & LOGI & AMZN & AAPL & \% Rend. Anual & Desv. Est. Anual \\ \cline { 2 - 8 } GOOG & 1 & & & & 8.0% & 28.7 \\ CSCO & 0.43 & 1 & & & & 7.5% & 36.3 \\ LOGI & 0.34 & 0.28 & 1 & & & 6.0% & 46.2 \\ AMZN & 0.55 & 0.34 & 0.35 & 1 & & 12.5% & 34.0 \\ AAPL & 0.62 & 0.43 & 0.39 & 0.58 & 1 & 10.0% & 25.0 \end{tabular}

El resultado puede obtenerse utilizando las propiedades de la varianza para calcular Var(w1X+w2Y) y la relación: Cov(X,Y)=Cor(X,Y)Var(X)Var(Y)

Estudia mejor, ¡ahora en español!

Entiende todos los problemas con explicaciones al instante y pasos fáciles de aprender de la mano de expertos reales.